Beyond Debt

Image: Christ Driving the Money Changers from the Temple

Soundtrack: Comrade Jesus Christ - Kev Carmody (1988, Australia)

Watch: The Shock Doctrine

Learn: islamicmarkets.comLast time in W: House of Cards, I explored how debt creates systemic risk, building upon W: The Big Squeeze's speculation. It's one thing to recognize the Boom and Bust Business Cycle and the Barons who gain from it, but it's often taken as a necessary part of the way the world works; Much the same way that most people saw slavery before its [relative] abolition.

If history shows anything, it is that there’s no better way to justify relations founded on violence, to make such relations seem moral, than by reframing them in the language of debt—above all, because it immediately makes it seem that it’s the victim who’s doing something wrong. - Debt: The First 5000 Years

Debt is a system that is applied to everyone, from individuals to nation-states. It is used to manufacture markets that deteriorate into fascism. It is used in the process of making someone a slave, whether it be considered an indebtment to society or creditors, enforced by the [military | police | prison] industrial complex. Through its grading of fees, it's a system that weighs the heaviest for those on the bottom as people on the top push for growth at all costs.

If we have become a debt society, it is because the legacy of war, conquest, and slavery has never completely gone away. It’s still there, lodged in our most intimate conceptions of honor, property, even freedom. It’s just that we can no longer see that it’s there.

While these ideas of the marketplace built on violence were born in the very nature of the civilization itself, there has also been a long history of people choosing different paths; This was a path once shared by all Abraham's children.

While the details of the larger story, challenging large parts of the modern manufactured mythos, are undoubtedly worthy of telling, today, I am sharing the punchline of my last six months of research; A way for the average person to ethically invest while living in a world of violence. And no, it's not the indelibility or speculation of crypto.

Islamic Revival

In the 1970s, as Keynesian economics began to fail noticeably, the powers of the Westen World would turn to Milton Friedman and his equally flawed neoliberal ideology. These policies would be applied both domestically and abroad to the unconsenting public after periods of, often manufactured, Economic Shock to unwind much of the equality gains of the "50s, ushering a new era of global authoritarianism through the use of the market.

After Margaret Thatcher and Ronald Reagan took power, the rest of the package soon followed: massive tax cuts for the rich, the crushing of trade unions, deregulation, privatisation, outsourcing and competition in public services. Through the IMF, the World Bank, the Maastricht treaty and the World Trade Organisation, neoliberal policies were imposed – often without democratic consent – on much of the world.

In response to these decline social-economics and increasing military action, the Islamic World began to return to the basics of the Patriarchal Abrahamic teachings, including revitalizing anti-usury and anti-speculative accounting dominating the now Judeo-Christian-led world. This spawned a new, but not entirely separate, financial system founded on Shariah law.

While manufacturing consent tends to present Muslims in a certain light, the core tenants of Shariah are values-based approaches focused on harm reduction while taking into consideration hardship and intent. By navigating rules as a system of tiered values, this rule-making system presents as something that is much more tolerant than the casuistic laws they initially replaced; Something our punitive-justice system could undoubtedly learn from.

For example, the abstinence of pork is a rule, but it’s not absolute. This restriction is ranked below the need for proper nutrition; choosing to starve, or be malnourished, would create more significant hardship.

Allah intends every facility for you, and he does not want to put you in hardship - Qur'an 2:185

He (Allah) has not laid down upon you in religion any hardship - Qur'an 22:78

With the Qur'an and Hadith, I would suggest that Muhammad understood not just the flexibility of circumstance but that in a Buddist sense to abstain from suffering by casting aside doubt/worry and favoring the present.

Whenever one doubts and does not know whether one prays three or four raka'at such person should act on certainty and ignore the doubts - The Hadith

While the Protestant entangled Free Market view espouses trust in God’s Invisible hand, the Islamic approach instead takes responsibility. It considers the impacts on the community, such as pollution or violence, as first-order importance while permitting flexibility to choose the most ethical option available.

Trust in God, But Tie Your Camel - Mohammed

So while [ usury | interest ] is generally not permitted, if you live in an area where the only way to buy a home is through a mortgage or be subjected to a lifetime of renting, it's then acceptable to get a mortgage; With the expectation that you change to a better option when it comes available. This could mean either refinancing to a lower interest rate or ideally switching to something that looks more like a fixed-cost lease-to-purchase agreement.

On the other hand, it would not be permittable to issue a mortgage because that’s unnecessarily harmful where you could otherwise provide a fix-cost agreement.

These rules created a patchwork of financial systems spread across the world, starting in Egypt in the "70s but also spring up in places like Indianapolis, IN, in the "80s.

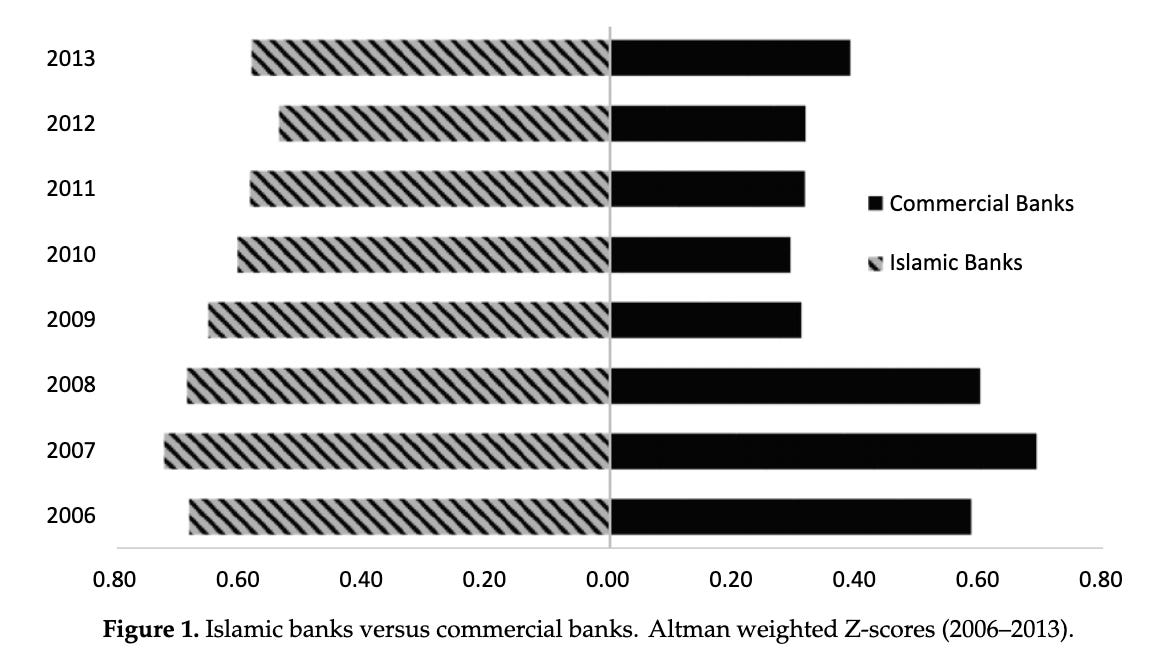

By avoiding usury, and therefore debt by favoring profit-sharing agreements, these institutions grew in a collaborative environment only to prove that during the 2008 Speculative Financial Crash, they were more resilient than their commercial peers.

While this chart looks at the resiliency of banks focused in the Middle East, S&P maintains Shariah compliant versions of their significant indices for comparison.

As I've described, the application of Shariah is highly situational and open to interpretation. Still, they generally can be described as only own stocks in companies with below one-third indebtedness while avoiding those who derive more than 5% of their revenue from haram activities like alcohol, firearms, tobacco, [ gambling | speculation | financial ], pork, and sex work.

By default, most stock charts focus on price, as most customers are speculators; since Shariah favors profit-sharing, it’s more accurate to look at total returns, which is [ Price + Dividends | Cost + Profit-Sharing ].

While this shouldn't be considered robust as a backtest, I have checked these results across multiple shariah pairings in various markets over the last six months and found these results to be generally consistent. Shariah will typically outperform baseline in the medium to long term but not necessarily keep up with the highest growers.

While I don’t consider profits the primary, a system with a gambler’s addiction to chasing profits at the expense of others would be impossible to leave if the transition was not made to be accessible and sustainable.

Surely Allah introduced the religion as easy, full with kindness and wide. He did not make it narrow - The Hadith

One of the notable things about investing in equities that do not have exposure to high levels of debt is that one is protected from some of the hostile activity that [ Vulture Capitalists | Private Equity ] can inflict on companies.

Similarly, the Supreme Court has reaffirmed multiple times, and most recently, with Hobby Lobby, a fiduciary duty does not mean that one has to maximize profit. Shareholder value is considered more abstract and not directly correlated with earnings; Anyone who says differently is just trying to abdicate social responsibility.

After 50 years, the Islamic banking system has grown to manage about $2.05 trillion [2017], or a little over 1% of the world's banking assets, making it about the size of HSBC. A number whose growth is sure to be supported with Chinese "Belt" investments into the Silk Road.

The Long Now

While the transition from a [ violence | debt | slavery ] system is undoubtedly going to take time, for those of us who have savings and retirement accounts, we can choose to use our administrative power in better ways than the hegemonic default.

Unified Management Corporation started one of the first Islamic Mutual Funds in Indianapolis, and it's still in operation today as Amana Mutual Funds Trust by Saturna Capital. And as far as I can tell, they are the only public-service provider in the US.

While not as technologically sophisticated as a Betterment or Wealthfront, or as cost-efficient as Vanguard, these funds do something that other Social Responsible ESGs don't; they avoid speculation and debt, the fundamental game mechanics that prop up this extractive system in the first place. And they do it with decades of developed expertise founded on making ethical choices long before it became the popular way to raise a fund on Wall Street.

By starting with the question, how can we ethically invest through collaboration, instead of focus solely on maximizing profits, a level of due diligence that naturally slower and more considered is encouraged. This tends to protect against systemic levels of fraud that indices can’t while not playing to the momentum-based bubbles of retail and hedge funds.

For comparison, here is a breakdown of these funds compared to some standard benchmarks; Color-coded by category.

It's important to note that the expense ratios are much higher, which does have negative compounding effects in the long term. However, they are much higher because these funds are much smaller while supporting a more considered due diligence process. As such, these ratios have been coming down over the years and should continue to do so as the funds grow in size. Which is a bit different than Fididity hiding a $102 annual recorded keeping fee in my 401k for the pleasure of electronically routing my money into their underlying funds.

With that in mind, if you look at the Growth fund vs. the benchmark stock ETFs, it does outperform in the current market base and look strong over the long term, including 2008.

The Developing World and Bonds do have below benchmark during the first few periods, but this is expected as these new funds get off the ground and stabilize with their process over the coming years.

Now a portfolio, retirement or otherwise, should be a balance of funds. While other services will balance these for you automatically, Saturna is a little more old school. You have to do it yourself by simply buying in proportionally, but they do provide a quiz that you can take to figure out what blend you want to aim for.

For reference, here are the blended stats. In cases where the underlying fund is newer than the extended timeline, I defaulted to the inception average to estimate the missing data. Past performance is no guarantee of future results.

I recommend reading through their provided materials with the funds. The Statement of Additional Information covers their voting and social responsibility policies and the compensation schedule. In addition to not supporting loans, they also don’t engage in real estate.

The Quarterly Commentaries expose how much underlying debt exists in the portfolios, with the highest being 15.9% on Income, 12% on Developing World, 10% on Growth.

While I could not find accurate index-wide data; For context, Apple and Microsoft have less than 5%, while GameStop, before the recent rally, was looking at 82%. The big-name auto manufacturers are between 49.4-76.9% indebted, with the mean of most industry sectors at around 20%. Based on my sampling I expect the distribution of debt as stacked onto companies the way it stacked on people; considering the difference between getting small business loans and startups.

This speaks to the underlying companies' debt burden and does not include the additional pricing exposure due to other forms of system debt, like margin traders that I explored in W: House of Cards.

The master’s tools will never dismantle the master’s house. - Audre Lorde

Today, I sit as someone who has paid more to financiers in interest than I will ever pay to the university that was already overcharging for my low-status degree, something that I will have to continue to serve for years to come. So while the calls to cancel student debt mount, that is but a step on the horizon; The future resides in abolishing debt, and for me, that starts now.

السلام عليك

The above references an opinion and is for information purposes only. It is not intended to be investment advice. Seek a duly licensed professional for investment advice.